Key Takeaways:

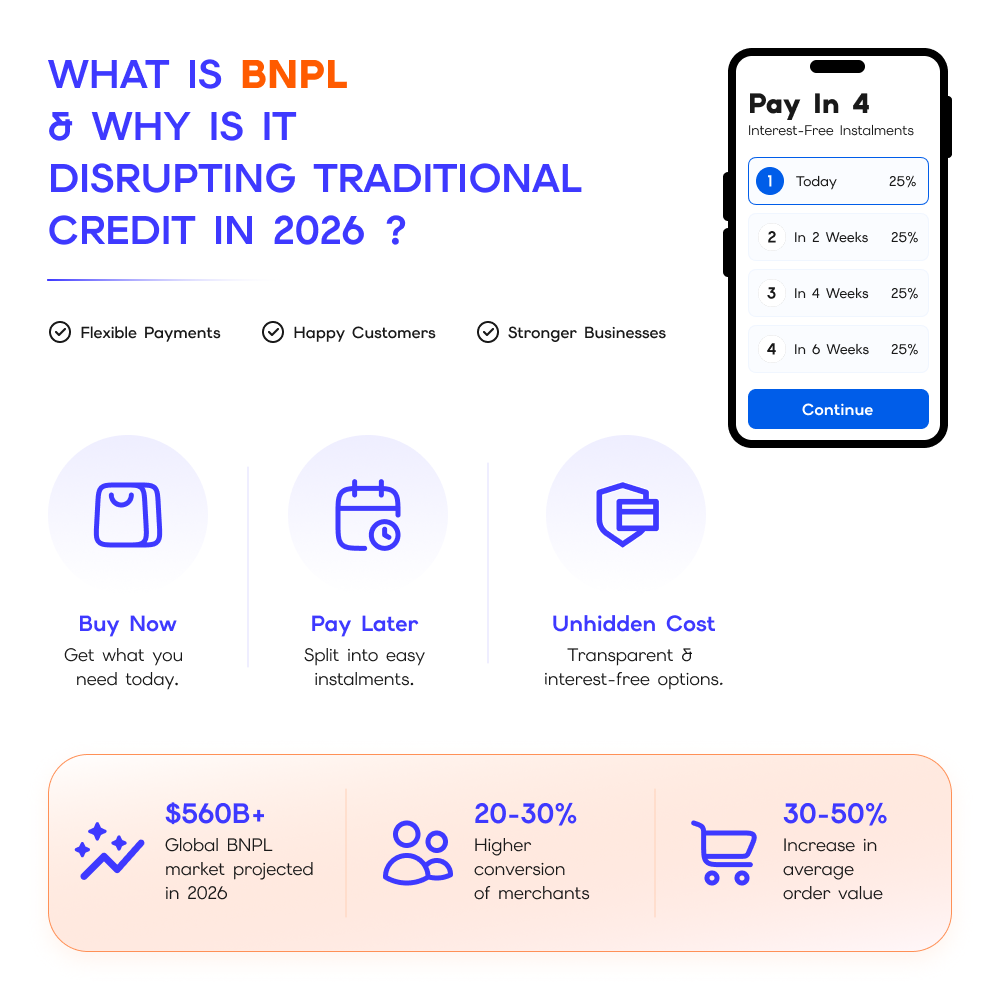

- The global BNPL market is expected to cross $560+ billion by 2026 with rapid fintech adoption.

- Merchants using BNPL see 20–30% higher conversion rates and up to 50% bigger cart values.

- AI-powered underwriting enables instant approvals using real-time behavioral and transaction data.

- BNPL is expanding beyond retail into healthcare, travel, education, and B2B payments.

- Compliance with RBI, KYC, AML, PCI-DSS, and CFPB regulations is now essential for BNPL platforms.

- Enterprise BNPL apps use microservices, embedded finance APIs, and virtual cards for scalable growth.

The global financial ecosystem is undergoing a major transformation, and Buy Now Pay Later (BNPL) platforms are sitting at the center of this disruption. Consumers no longer want lengthy loan approvals, hidden credit card charges, or rigid repayment structures. They want flexibility, speed, transparency, and a digital-first experience that feels effortless across mobile and web platforms. This demand has turned BNPL into one of the fastest-growing fintech business models in the world.

For startups, financial institutions, retailers, and fintech enterprises, investing in BNPL app development in 2026 is no longer just an innovation strategy it is a competitive necessity. From AI-driven underwriting to embedded finance and virtual card issuance, BNPL applications are reshaping how consumers purchase products online and offline.

What Is BNPL and Why Is It Disrupting Traditional Credit in 2026?

Buy Now Pay Later (BNPL) is a short-term financing model that allows consumers to purchase products immediately while paying for them over time through installments. Unlike traditional credit cards or personal loans, BNPL platforms provide faster approvals, lower friction, transparent repayment schedules, and often interest-free installment plans.

The rise of digital commerce, mobile-first consumers, and embedded finance ecosystems has accelerated BNPL adoption worldwide. Younger consumers, especially Gen Z and Millennials, increasingly prefer BNPL solutions because they offer convenience without the complexities associated with traditional banking products.

A major reason BNPL is disrupting legacy credit systems is its accessibility. Traditional credit cards often require extensive documentation, credit history, and lengthy approval cycles. BNPL apps, however, use AI-powered risk assessment engines, behavioral analytics, transaction history, and alternative data to evaluate borrowers in seconds.

In 2026, BNPL is evolving beyond retail purchases. Consumers are now using installment financing for healthcare, education, travel, electronics, insurance premiums, home improvement services, and even B2B purchases. This expansion has transformed BNPL from a niche fintech product into a mainstream digital lending ecosystem.

According to market reports by Grand View Research and Statista, the global BNPL market is projected to surpass hundreds of billions of dollars in transaction value by 2026, driven by rising smartphone penetration and e-commerce growth.

A real-world example of this disruption can be seen in how younger users avoid traditional credit cards altogether. Instead of opening a credit line with high interest rates, many consumers now use BNPL apps during checkout for transparent payment splitting and better spending control.

How BNPL Works: The Mechanics from User to Merchant to Lender

The operational structure of a BNPL ecosystem involves three major participants: the consumer, the merchant, and the financing provider. Understanding this flow is critical for businesses planning to invest in BNPL app development services.

When a customer selects a product online or in-store, the BNPL option appears during checkout. The user chooses a repayment schedule, typically split into weekly or monthly installments. The BNPL platform instantly evaluates eligibility using credit scoring algorithms and alternative financial data.

If approved, the merchant receives the full payment upfront from the BNPL provider, minus a merchant transaction fee. The customer then repays the amount over time according to the agreed schedule.

This model benefits all stakeholders involved:

- Consumers receive flexible financing with minimal friction.

- Merchants experience higher conversions and increased order values.

- BNPL providers generate revenue through merchant fees, subscriptions, and late charges.

The technology behind this process includes:

- Real-time risk engines

- Payment gateway integrations

- Credit bureau APIs

- KYC verification systems

- Fraud detection layers

- Banking infrastructure APIs

- Automated repayment schedulers

In modern BNPL ecosystems, APIs and microservices architecture enable instant decision-making within milliseconds. This seamless experience is what differentiates BNPL platforms from traditional banking applications.

BNPL Market Size and the Key Players (Klarna, Afterpay, Affirm)

The BNPL market has become one of the most competitive sectors in fintech. Companies like Affirm, Afterpay, and Klarna have transformed consumer financing by creating intuitive and merchant-friendly installment payment systems.

Klarna, for example, expanded rapidly across Europe and North America by integrating deeply into e-commerce ecosystems. Affirm differentiated itself by offering transparent installment plans without hidden fees, while Afterpay became highly popular among younger retail shoppers.

Global BNPL Growth Statistics

|

Metric

|

Estimated Value in 2026

|

|

Global BNPL Market Value

|

$560+ Billion

|

|

CAGR Growth Rate

|

20%+

|

|

Top BNPL User Demographic

|

Gen Z & Millennials

|

|

Average Conversion Increase for Merchants

|

20–30%

|

|

Average Increase in Cart Size

|

30–50%

|

The rise of embedded finance and digital wallets is further accelerating BNPL adoption. Major technology companies, payment providers, and banks are now integrating BNPL directly into their ecosystems.

A notable real-life scenario occurred during major online shopping events where merchants offering BNPL observed significantly lower cart abandonment rates compared to stores without installment options.

Why Merchants Love BNPL: 20–30% Higher Conversion Rates

Merchants across industries increasingly adopt BNPL because it directly impacts revenue growth. The ability to spread payments across installments encourages customers to complete purchases they might otherwise postpone.

Studies show that merchants integrating BNPL often experience:

- Higher conversion rates

- Increased average order value

- Lower cart abandonment

- Improved customer retention

- Greater purchase frequency

For example, a consumer considering a $629.39 smartphone may hesitate to pay the full amount upfront. However, when presented with a “Pay in 4 installments” option, the psychological purchase barrier decreases dramatically.

Fashion retailers, electronics brands, furniture businesses, healthcare providers, and travel platforms have all benefited from BNPL integration. The flexibility appeals particularly to digitally native consumers who prioritize convenience and cash-flow management.

An electronics retailer integrating BNPL into checkout observed a major increase in high-ticket purchases because consumers felt more comfortable splitting payments over several months.

Must-Have Features for a BNPL App

Building a successful BNPL application in 2026 requires more than simple installment management. Users expect intelligent financial experiences, frictionless onboarding, and enterprise-grade security.

.png)

A modern BNPL platform should include:

- AI-powered underwriting

- Real-time KYC verification

- Merchant dashboards

- Repayment automation

- Push notifications

- Fraud detection

- Virtual cards

- Multi-currency support

- Customer support modules

- Compliance management systems

The user experience must remain fast and intuitive while handling complex financial operations behind the scenes.

Instant Credit Scoring and Real-Time Eligibility Checks

One of the defining features of BNPL platforms is instant approval capability. Consumers expect financing decisions within seconds, not days.

Modern BNPL applications use:

- Banking transaction analysis

- Alternative credit data

- AI risk modeling

- Employment verification

- Spending behavior analytics

- Device intelligence

- Fraud indicators

Instead of relying solely on traditional credit bureaus, BNPL apps increasingly use machine learning to evaluate repayment probability.

For example, a first-time user without extensive credit history may still qualify based on salary inflow patterns, transaction consistency, and digital payment behavior.

This real-time scoring engine becomes the core differentiator of competitive BNPL platforms.

Frictionless Onboarding with Integrated KYC

Customer onboarding can determine whether users complete registration or abandon the application.

A frictionless onboarding flow typically includes:

- Mobile OTP verification

- Aadhaar/PAN verification

- OCR-based document scanning

- Face verification

- Liveness detection

- Bank account linking

In India, compliance with RBI digital lending guidelines requires strong identity verification and transparent disclosure practices.

A leading fintech platform reduced onboarding drop-offs significantly after implementing automated document scanning and real-time verification APIs.

Flexible Repayment Scheduling and Automated Reminders

Consumers choose BNPL because of repayment flexibility. Your application should allow multiple repayment structures, including:

- Weekly installments

- Bi-weekly installments

- Monthly EMIs

- Deferred payments

- Interest-free plans

- Subscription-linked repayment models

Automated reminders through SMS, email, push notifications, and WhatsApp integrations reduce missed payments and improve repayment rates.

Smart reminder systems powered by AI can even optimize notification timing based on user behavior.

Merchant Portal and E-Commerce Checkout Integration

Merchant integration is critical for BNPL scalability. Businesses require dashboards that provide visibility into transactions, approvals, settlements, disputes, and customer analytics.

Essential merchant-side capabilities include:

- Plugin integrations for Shopify and WooCommerce

- API-based checkout embedding

- Settlement reporting

- Refund management

- Sales analytics

- Chargeback monitoring

A seamless checkout experience directly impacts conversion rates and merchant adoption.

Virtual Card Issuance for In-Store BNPL

Virtual cards are becoming a major feature in BNPL ecosystems. These cards allow users to use installment financing even at offline retail locations.

By integrating with card networks like Visa and Mastercard, BNPL providers can issue temporary virtual cards for approved purchases.

This expands BNPL use cases into:

- Healthcare clinics

- Electronics stores

- Travel bookings

- Educational institutions

- Luxury retail

Virtual card issuance also enables omnichannel payment experiences.

In-App Dispute Resolution and Customer Support

Financial applications must prioritize customer trust. Disputes regarding refunds, repayment errors, or merchant issues can severely impact user retention if not handled effectively.

Modern BNPL apps include:

- AI chatbots

- Ticketing systems

- Live support

- Automated refund tracking

- Dispute escalation workflows

A strong customer support system improves platform credibility and regulatory compliance.

The Lending Engine: The Heart of Your BNPL App

The lending engine powers the financial intelligence of the BNPL platform. It determines approvals, risk exposure, installment structures, late fee handling, and repayment scheduling.

This engine requires sophisticated architecture capable of:

- Real-time underwriting

- Dynamic interest calculations

- Fraud monitoring

- Loan lifecycle management

- Compliance logging

- Portfolio analytics

Microservices architecture is increasingly preferred because it allows independent scaling of underwriting, payment processing, analytics, and notification systems.

AI-Powered Credit Risk Assessment and Soft Credit Bureau Pulls

Artificial intelligence is revolutionizing credit assessment in BNPL applications. Instead of rejecting users based solely on traditional credit scores, AI models analyze broader financial behavior.

A soft credit pull allows BNPL providers to assess financial eligibility without negatively impacting the user’s credit score.

This creates a less intimidating onboarding experience and encourages more users to apply.

AI-driven underwriting models evaluate:

- Spending patterns

- Bank cash flows

- Repayment consistency

- Device behavior

- Shopping habits

- Fraud risk signals

Companies using AI-based risk models have significantly reduced default rates while approving more users than traditional systems.

Late Fee Logic, Payment Cycle Management, and Default Handling

Repayment management is a critical aspect of BNPL operations. Poorly designed repayment systems can lead to customer dissatisfaction and regulatory scrutiny.

BNPL apps should support:

- Grace periods

- Partial payments

- Automated retries

- Payment restructuring

- Collections workflows

- Default prediction models

A real-world scenario can be seen in how major BNPL platforms proactively contact users before missed payments occur, reducing delinquency and improving customer relationships.

Transparent late fee disclosure is also becoming a legal requirement in several regions.

Compliance: Navigating BNPL Regulations in 2026

As BNPL adoption increases globally, regulators are tightening oversight around consumer protection, lending transparency, and responsible financing practices.

Compliance is no longer optional for BNPL platforms. Businesses must integrate legal frameworks into their technical architecture from the beginning.

Major compliance areas include:

- Consumer lending laws

- Data privacy regulations

- KYC/AML verification

- PCI-DSS compliance

- Credit reporting obligations

- Interest disclosure requirements

Ignoring compliance can lead to fines, license suspension, and reputational damage.

How CFPB Is Now Treating BNPL Like Credit Card Issuers (USA)

The Consumer Financial Protection Bureau (CFPB) has increased scrutiny of BNPL providers in the United States.

Regulators now expect BNPL companies to provide protections similar to credit card issuers, including:

- Transparent disclosures

- Dispute rights

- Refund protections

- Consumer reporting transparency

- Fee clarity

This regulatory shift reflects how mainstream BNPL has become within consumer finance.

Businesses planning global BNPL expansion must design flexible compliance architectures capable of adapting to changing laws.

KYC, AML, PCI-DSS, and Consumer Credit Laws by Region

BNPL applications process highly sensitive financial information, making security and compliance essential.

Key frameworks include:

|

Compliance Framework

|

Purpose

|

|

KYC

|

Identity verification and fraud prevention

|

|

AML

|

Prevention of money laundering activities

|

|

PCI-DSS

|

Protection of payment card data

|

|

GDPR

|

User data privacy in Europe

|

|

SOC 2

|

Security and operational compliance

|

|

Consumer Credit Laws

|

Lending transparency and borrower protection

|

Modern BNPL platforms use encrypted infrastructure, tokenized payment systems, and continuous fraud monitoring to maintain compliance.

BNPL Regulations in India: RBI Guidelines for Digital Lending

In India, the Reserve Bank of India has introduced stricter digital lending regulations impacting BNPL providers.

Key RBI expectations include:

- Transparent disclosure of fees

- Regulated lending partners

- Explicit borrower consent

- Secure data storage

- Direct fund disbursement

- Fair collection practices

Fintech companies must also ensure partnerships with licensed NBFCs or banks if they do not possess lending licenses themselves.

India’s rapidly growing digital payment ecosystem makes BNPL highly attractive, but compliance readiness is essential for long-term sustainability.

BNPL App Development Cost Breakdown

The cost of developing a BNPL application depends on:

- Feature complexity

- Regulatory requirements

- AI integration

- Geographic scope

- Infrastructure scalability

- Security architecture

- Team location

Development costs can vary significantly between MVPs and enterprise-grade platforms.

MVP ($30k–$80k): Basic Instalment Payments and KYC

An MVP BNPL application focuses on validating the business model quickly while minimizing development costs.

Typical MVP capabilities include:

- User registration

- KYC verification

- Basic underwriting

- Installment scheduling

- Payment gateway integration

- Merchant checkout integration

- Notification systems

This version is ideal for startups testing market demand.

Mid-Market ($150k–$300k): Multi-Currency, Advanced Risk Models

Mid-market BNPL platforms introduce more sophisticated infrastructure and scalability features.

These typically include:

- AI-based underwriting

- Multi-region compliance

- Multi-currency payments

- Advanced analytics

- Fraud detection

- Merchant dashboards

- Customer segmentation

- API ecosystems

This stage often supports regional expansion and higher transaction volumes.

Enterprise ($350k+): AI Underwriting, Virtual Cards, Microservices

Enterprise-grade BNPL platforms are designed for large-scale fintech operations.

They often include:

- Real-time AI underwriting

- Microservices architecture

- Distributed cloud infrastructure

- Virtual card issuance

- Embedded finance APIs

- Advanced compliance automation

- Data lakes and predictive analytics

Large enterprises prioritize scalability, uptime reliability, and cross-border regulatory management.

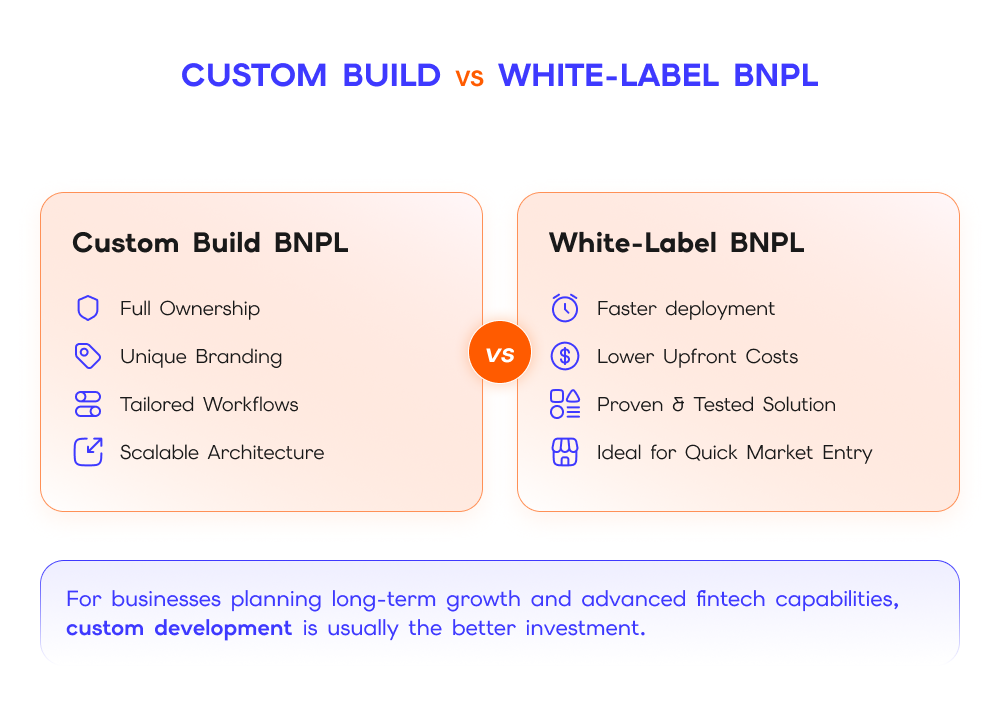

Custom Build vs. White-Label BNPL: Which Makes Sense for Your Business?

Choosing between custom development and white-label solutions depends on your business goals, timeline, and scalability requirements.

A white-label BNPL solution offers faster deployment and lower upfront costs. However, customization flexibility may be limited.

A custom-built BNPL application provides:

- Full ownership

- Unique branding

- Tailored workflows

- Scalable architecture

- Competitive differentiation

- Flexible integrations

For businesses planning long-term growth and advanced fintech capabilities, custom development is usually the better investment.

We help businesses evaluate both approaches and build secure BNPL ecosystems aligned with growth objectives.

BNPL Monetization Strategies: How to Make Money

BNPL platforms generate revenue through multiple monetization streams.

These include:

- Merchant transaction fees

- Late payment fees

- Subscription models

- Interest-bearing installment plans

- Consumer premium services

- Affiliate partnerships

- Data-driven insights

Successful BNPL businesses diversify monetization rather than relying solely on late fees.

Merchant Fees, Consumer Fees, Data Monetization, and Subscription Models

Merchant fees remain the primary revenue source for most BNPL providers. Merchants willingly pay these fees because BNPL improves conversion rates and average order values.

Additional monetization opportunities include:

- Premium consumer memberships

- Cashback partnerships

- Financial wellness subscriptions

- Credit-building services

- Personalized shopping recommendations

Some advanced fintech companies also use anonymized consumer behavior analytics to generate business intelligence for retailers while complying with privacy regulations.

Looking for BNPL App Development Experts?

Contact Us

Conclusion

Buy Now Pay Later applications are no longer experimental fintech products. They have become a core part of the digital commerce ecosystem in 2026. Consumers expect flexible financing experiences integrated seamlessly into mobile apps, e-commerce platforms, and in-store purchases.

However, building a successful BNPL platform requires far more than installment functionality. Businesses need robust underwriting systems, AI-powered risk engines, enterprise-grade compliance architecture, secure payment infrastructure, merchant ecosystems, and scalable cloud-native development.

Companies entering the BNPL market today must focus equally on user experience, financial compliance, fraud prevention, and long-term scalability.

At TechQware Technologies, we specialize in fintech app development services, digital lending platforms, AI-driven financial applications, and scalable embedded finance ecosystems. Whether you are building an MVP or launching a global enterprise BNPL platform, our team can help you design, develop, and deploy a secure and future-ready solution tailored to your business goals.

If you are planning to launch a next-generation BNPL app in 2026, now is the ideal time to invest in a platform that combines compliance, intelligence, and exceptional user experience.

FAQs

How does a BNPL app make money?

BNPL apps primarily generate revenue through merchant transaction fees. Additional income streams may include late fees, subscription plans, premium financial services, interest-bearing installment plans, and affiliate partnerships.

Is building a BNPL app safe and compliant?

Yes, BNPL applications can be highly secure and compliant when built with proper regulatory frameworks, encrypted infrastructure, fraud detection systems, PCI-DSS compliance, and strong KYC/AML verification processes.

How long does it take to build a BNPL app?

A basic MVP BNPL application may take approximately 4–6 months to develop, while enterprise-grade platforms with AI underwriting, virtual cards, and multi-region compliance can require 12 months or more.

What is a soft credit pull and how is it used in BNPL?

A soft credit pull is a credit assessment method that allows lenders to evaluate a user’s financial profile without negatively affecting their credit score. BNPL providers commonly use soft pulls for instant eligibility checks.

How is BNPL regulated in India in 2026?

In India, BNPL platforms are regulated under RBI digital lending guidelines that require transparent fee disclosure, secure data practices, borrower consent mechanisms, and partnerships with licensed NBFCs or banks.

Can I build a BNPL app without a lending license?

Yes, many fintech startups partner with licensed banks or NBFCs to provide lending infrastructure while focusing on technology, user experience, and merchant integration.

TechQware

TechQware

.png)