Key Takeaways:

- The neobanking market is projected to exceed $210 billion with growing demand for digital banking.

- Businesses can launch neobanks using BaaS, White-Label, or custom development models.

- A scalable neobank requires microservices architecture, API-first development, and strong security.

- Compliance with KYC/AML, PCI-DSS, GDPR, and RBI regulations is essential.

- MVP development costs typically range from $40k–$70k.

The financial services landscape is undergoing one of the most dramatic transformations in its history, and neobanks are at the center of this disruption. With digital-first experiences, lower operational costs, and customer-centric innovation, neobanks are redefining how users interact with money. For businesses looking to enter fintech, building a neobank is no longer just an ambitious idea it’s a strategic opportunity.

In this comprehensive guide by our team, we will walk you through everything you need to know about building a neobank app from scratch, including architecture, features, compliance requirements, cost breakdown, and monetization strategies. This guide is crafted to help founders, product managers, and enterprises make informed decisions while building scalable, secure, and compliant digital banking solutions.

What Is a Neobank and How Is It Different from a Digital Bank?

A neobank is a fully digital financial institution that operates without physical branches and delivers banking services entirely through mobile apps or web platforms. Unlike traditional banks, neobanks are built on modern tech stacks, leveraging APIs, cloud infrastructure, and automation to deliver seamless financial experiences.

Digital banks, on the other hand, are typically extensions of traditional banks that have digitized their services but still rely on legacy infrastructure and branch networks. The key distinction lies in the foundation neobanks are “born digital,” while digital banks are “digitally transformed.”

Neobanks prioritize speed, UX, and personalization. They eliminate paperwork, reduce onboarding friction, and provide real-time insights into spending. A real-life example is how users can open an account in under 5 minutes with digital KYC, compared to days in traditional banking systems.

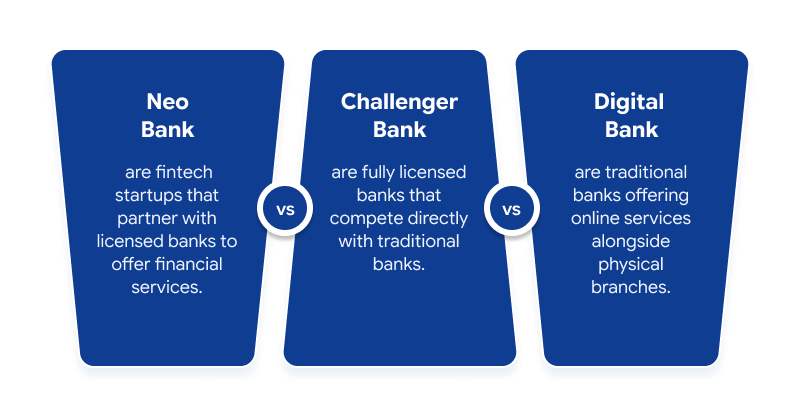

Neobank vs. Challenger Bank vs. Digital Bank: Key Distinctions

While these terms are often used interchangeably, they represent different business and operational models.

- Neobanks are fintech startups that partner with licensed banks to offer financial services.

- Challenger banks are fully licensed banks that compete directly with traditional banks.

- Digital banks are traditional banks offering online services alongside physical branches.

- Challenger banks have regulatory independence, while neobanks rely on sponsor banks. This distinction significantly impacts compliance, cost, and scalability.

A well-known scenario is a fintech startup launching quickly using a Banking-as-a-Service provider, whereas a challenger bank may take years to obtain licenses and build infrastructure.

Why the Global Neobanking Market Is Projected to Exceed $210 Billion

The explosive growth of neobanking is driven by multiple macroeconomic and technological factors. Increasing smartphone penetration, demand for frictionless banking, and dissatisfaction with traditional banks are accelerating adoption.

A key fact is that over 70% of millennials prefer digital banking experiences over traditional ones. Additionally, SMEs are rapidly adopting neobanks for faster payments, better analytics, and lower fees.

In emerging markets like India, financial inclusion initiatives and digital identity systems such as Aadhaar are further boosting neobank adoption. The combination of regulatory support and technological infrastructure is creating a fertile ground for growth.

Three Models for Building a Neobank: From Scratch, BaaS, or White-Label

When building a neobank, choosing the right model is one of the most critical decisions. Each approach comes with its own trade-offs in terms of control, cost, and time-to-market.

|

Model

|

Time to Market

|

Cost

|

Flexibility

|

Compliance Burden

|

|

From Scratch

|

High

|

High

|

Very High

|

High

|

|

BaaS

|

Medium

|

Medium

|

High

|

Medium

|

|

White-Label

|

Low

|

Low

|

Limited

|

Low

|

Building from Scratch: Full Control, Longer Timeline, Higher Cost

Building a neobank from scratch offers complete control over your technology stack, user experience, and business logic. However, this approach requires significant investment in engineering, compliance, and infrastructure.

A real-world example is when fintech startups attempt to build proprietary ledger systems. While this provides flexibility, it also introduces complexity in maintaining transactional integrity and compliance.

This model is best suited for enterprises with long-term vision, strong funding, and in-house technical expertise.

Banking-as-a-Service (BaaS): Solaris, Synapse, Railsr Explained

Banking-as-a-Service platforms allow fintech companies to integrate banking functionalities through APIs without becoming licensed banks themselves. Providers like Solaris, Synapse, and Railsr handle regulatory compliance, account management, and payment processing.

This model accelerates time-to-market and reduces regulatory overhead. For example, a startup can launch debit card services within months by integrating BaaS APIs instead of building infrastructure from scratch.

White-Label Platforms: Fastest to Market, Least Flexible

White-label solutions offer pre-built neobank platforms that can be customized with your branding. While this approach enables rapid deployment, it limits customization and scalability.

This model is ideal for businesses testing the market or launching MVPs quickly. However, as the business grows, migrating to a more flexible architecture becomes necessary.

Core Architecture for a Production-Ready Neobank

A robust architecture is the backbone of any successful neobank. It must be scalable, secure, and capable of handling millions of transactions in real time.

Why Microservices Are Non-Negotiable (Revolut’s Monolith Mistake)

Microservices architecture allows independent deployment and scaling of different components such as payments, user management, and notifications. This modular approach enhances system resilience and agility.

A well-known case is when fintech platforms initially built monolithic systems and later struggled with scalability, forcing costly migrations to microservices.

Core Banking Engine: Ledger, Payments, Cards, and Analytics

The world of neobanking isn't just about sleek apps and neon-colored plastic; it’s a high-stakes balancing act between cutting-edge tech and rigid legal frameworks. To survive, these digital-first banks must master four critical pillars of compliance.

The Compliance Quadrant

|

Regulation

|

Primary Focus

|

Key Requirement

|

|

AML & KYC

|

Financial Integrity

|

Verifying identities and flagging "shady" transaction patterns.

|

|

PCI-DSS

|

Card Security

|

Hardening the digital vault where credit/debit card data lives.

|

|

GDPR

|

Data Sovereignty

|

Giving users the "Right to be Forgotten" and total privacy.

|

|

RBI (India)

|

Local Governance

|

Keeping Indian data on Indian soil and following strict lending caps.

|

1. The Financial Gatekeepers: AML & KYC

Neobanks aren't just moving money; they are the front line against financial crime. Under Anti-Money Laundering (AML) rules, they act as digital detectives. By using Know Your Customer (KYC) protocols, they ensure that "John Doe" is actually John Doe and not a shell company funneling illicit funds.

2. The Fort Knox of Data: PCI-DSS

If you handle 16-digit card numbers, you play by the PCI-DSS rules. For a neobank, this means:

- End-to-End Encryption: Making data unreadable to hackers.

- Vulnerability Scans: Constantly poking holes in their own systems to find weaknesses before the bad guys do.

3. Privacy as a Human Right: GDPR

Under GDPR, a neobank doesn't "own" your data they just borrow it. Users have the power to audit what the bank knows about them. If a neobank fails to protect this privacy, the fines can reach up to 4% of their global annual turnover, which is enough to sink even the most successful startup.

4. The Indian Playbook: RBI Guidelines

In India, the Reserve Bank of India (RBI) sets the gold standard. Neobanks (which often partner with traditional banks) must navigate:

- Data Localization: Ensuring that financial data stays within Indian borders.

- Digital Lending Limits: Strict transparency on interest rates and recovery practices to protect the everyday borrower.

The Bottom Line: Compliance isn't a "check-the-box" chore it's the foundation of Customer Trust. In an industry where you can't walk into a physical branch to complain, your reputation is only as strong as your last security audit.

API-First Design and Third-Party Integrations (Payment Rails, KYC)

An API-first approach ensures seamless integration with third-party services such as payment gateways, KYC providers, and fraud detection systems.

For example, integrating UPI in India allows instant payments, significantly enhancing user experience.

Cloud Infrastructure: AWS/GCP/Azure with ACID-Compliant Databases

Cloud platforms provide scalability, reliability, and cost efficiency. Using managed services ensures high availability and disaster recovery.

Databases must support ACID properties to maintain consistency in financial transactions. This is crucial for regulatory compliance and user trust.

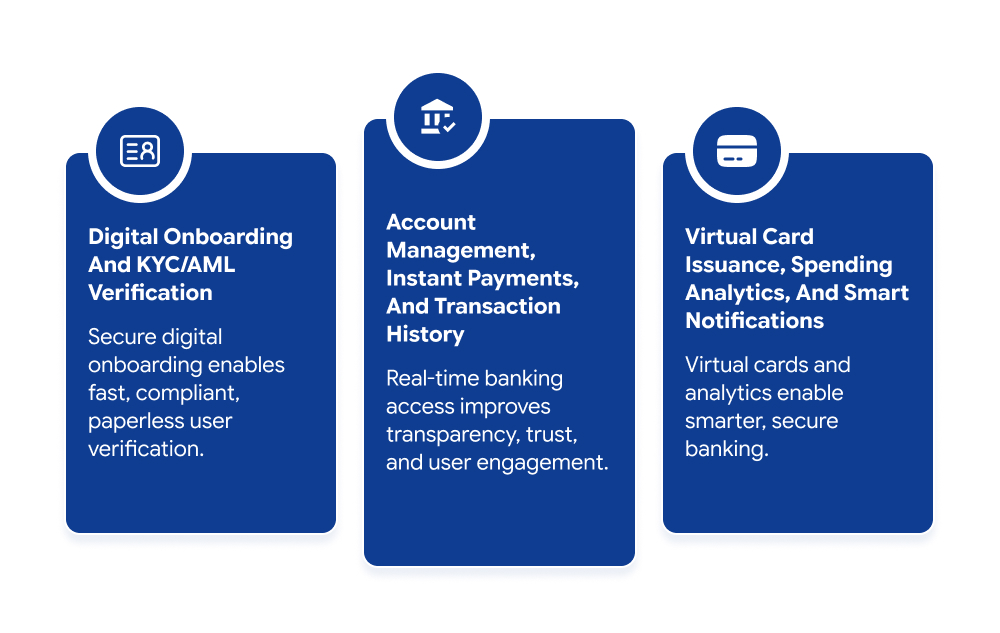

Must-Have Features for a Neobank MVP

An MVP should focus on delivering core functionalities while ensuring a seamless user experience.

Digital Onboarding and KYC/AML Verification

Digital onboarding should be fast, secure, and compliant. Features include:

- Document verification

- Facial recognition

- OTP-based authentication

A real-life example is onboarding users within minutes using eKYC, eliminating the need for physical verification.

Account Management, Instant Payments, and Transaction History

Users should be able to:

- View balances in real time

- Transfer funds instantly

- Access detailed transaction history

This transparency builds trust and enhances user engagement.

Virtual Card Issuance, Spending Analytics, and Smart Notifications

Virtual cards enable secure online transactions, while analytics provide insights into spending patterns.

Smart notifications keep users informed about transactions, helping prevent fraud and manage finances effectively.

Regulatory and Compliance Requirements for Neobanks

Compliance is one of the most complex aspects of building a neobank. It involves adhering to multiple regulations across jurisdictions.

Banking License vs. Sponsor Bank Model: Which Path Is Right for You?

Obtaining a banking license offers independence but requires significant capital and time. Partnering with a sponsor bank allows faster entry but limits control.

The choice depends on your business goals, funding, and risk appetite.

AML, PCI-DSS, GDPR, and RBI Regulations (India-Specific)

Neobanks operate in a highly regulated environment, and complying with key financial and data protection standards is essential to ensure both legal validity and customer trust.

AML (Anti-Money Laundering) regulations require neobanks to monitor transactions, verify customer identities, and report suspicious activities to prevent illegal financial flows such as money laundering or terrorist financing. This involves continuous transaction screening and risk profiling.

PCI-DSS (Payment Card Industry Data Security Standard) focuses on securing card-related data. Neobanks must implement strict controls like encryption, secure networks, and regular security audits to protect users’ card information from breaches and fraud.

GDPR (General Data Protection Regulation) ensures that user data is collected, stored, and processed transparently and securely. It gives users control over their personal data, including rights to access, modify, or delete their information.

In the Indian context, compliance with RBI (Reserve Bank of India) guidelines is mandatory. These include KYC norms, data localization requirements, digital lending regulations, and cybersecurity frameworks specific to financial institutions operating in India.

Failure to comply with these regulations can lead to severe financial penalties, legal action, operational restrictions, and reputational damage, which can significantly impact user trust and long-term business sustainability.

RegTech Tools for Automated Compliance Monitoring

RegTech (Regulatory Technology) tools play a crucial role in modern neobanking by automating complex compliance workflows that would otherwise require extensive manual intervention. Instead of relying on periodic checks, these tools operate continuously in the background, ensuring that every transaction and user activity aligns with regulatory requirements.

They use advanced analytics, rule engines, and AI models to monitor transactions in real time, flag suspicious patterns, and perform automated AML (Anti-Money Laundering) checks. For instance, if a user’s transaction behavior suddenly deviates from their usual pattern or matches known risk indicators, the system can instantly generate alerts or trigger further verification.

In addition to monitoring, RegTech platforms also streamline reporting and audit processes by automatically generating compliance reports required by regulators. This not only reduces human error but also ensures timely submissions, which is critical for avoiding penalties.

Overall, RegTech tools help neobanks stay compliant at scale by reducing operational costs, improving accuracy, and enabling faster response to regulatory changes, making them an essential part of any fintech infrastructure.

Security Architecture for a Neobank

A modern neobank relies on a zero-trust security architecture built around the idea of “never trust, always verify.” Every user, device, application, and request must undergo continuous authentication and authorization before gaining access to any system or sensitive data whether the request originates internally or externally. This minimizes the chances of insider misuse, unauthorized access, and lateral cyberattacks across the banking ecosystem.

To strengthen identity and access management, OAuth 2.0 enables secure, token-based authentication without exposing user credentials. Instead of sharing passwords with third-party applications, users authorize access through encrypted tokens that carry specific permissions and limited validity periods. This approach reduces credential theft risks, enhances session security, and provides more controlled access management.

Another critical layer of protection comes from certificate pinning, which ensures that the neobank application communicates only with authenticated and pre-approved servers. By validating server certificates directly within the app, certificate pinning effectively blocks man-in-the-middle attacks, preventing cybercriminals from intercepting or altering sensitive financial data—even when users connect through unsecured or public networks.

Together, zero-trust architecture, OAuth 2.0, and certificate pinning create a highly resilient security framework for neobanking platforms. This multi-layered approach safeguards customer information, secures digital transactions, and helps maintain user trust in an increasingly high-risk financial landscape.

Zero-Trust Principles, OAuth 2.0, and Certificate Pinning

Zero-trust architecture is built on the principle of “never trust, always verify,” meaning every user, device, and request must be authenticated and authorized continuously regardless of whether it originates inside or outside the network. In a neobank, this ensures that even internal systems cannot freely access sensitive data without strict validation, reducing the risk of insider threats and lateral attacks.

OAuth 2.0 strengthens this by enabling secure, token-based authentication, allowing users to grant limited access to apps without sharing credentials. Instead of exposing passwords, the system uses access tokens with defined scopes and expiration, which minimizes the attack surface and improves session security.

Certificate pinning adds another critical layer by ensuring that the app only communicates with trusted servers whose certificates are pre-verified. This prevents attackers from intercepting or altering data through man-in-the-middle attacks, even if a user is on an unsecured network.

Together, these mechanisms create a multi-layered security framework that protects user data, secures transactions, and maintains trust in high-risk financial environments like neobanking.

AI-Powered Fraud Detection and Real-Time Transaction Monitoring

AI-powered fraud detection in neobanking goes far beyond simple rule-based systems by continuously learning from user behavior and transaction data. These models analyze patterns such as transaction frequency, location, device usage, and spending habits to establish a “normal behavior baseline” for each user.

When a transaction deviates from this baseline such as a sudden high-value purchase, login from a new location, or multiple rapid transactions the system instantly flags it as suspicious. Based on the risk score, the system can trigger real-time actions like sending alerts, requesting additional authentication (OTP/biometric), or temporarily blocking the transaction to prevent potential fraud.

For example, if a user who typically makes small local payments suddenly initiates an international transaction at an unusual hour, the AI system can detect this anomaly within milliseconds and intervene before the transaction is completed. This proactive approach significantly reduces fraud losses while maintaining a seamless user experience for legitimate transactions.

Neobank App Development Cost in 2026

The cost of building a neobank app in 2026 is not fixed, as it depends heavily on the depth of features, architectural complexity, regulatory requirements, and integrations involved. A simple MVP with essential banking capabilities like onboarding, KYC, and fund transfers can be built within a controlled budget, while a full-scale neobank with lending, investments, multi-currency support, and AI-driven analytics requires significantly higher investment.

One of the biggest cost drivers is architecture choice. A microservices-based, cloud-native system built on platforms like AWS or GCP demands more upfront engineering effort but ensures long-term scalability and performance. In contrast, simpler architectures may reduce initial costs but can lead to expensive rework as the user base grows.

Another major factor is compliance and security. Meeting standards such as KYC/AML, PCI-DSS, and region-specific regulations (like RBI guidelines in India) involves third-party integrations, audits, and continuous monitoring systems, all of which add to development and operational costs.

Additionally, third-party integrations including payment gateways, card issuers, fraud detection tools, and Banking-as-a-Service providers introduce both setup and recurring costs. The more advanced your feature set, the more dependencies you’ll need to manage.

In short, while costs can start relatively lean for validation purposes, building a production-ready, scalable, and compliant neobank requires strategic investment across technology, security, and regulat.

MVP ($40k–$70k): Accounts, Transfers, KYC

At the MVP stage, the objective is not to build a feature-heavy banking platform but to create a lean, reliable, and compliant foundation that proves your neobank’s core value proposition in the market. This phase is all about validating whether users trust your product enough to onboard, transact, and return.

An MVP typically includes three mission-critical pillars:

1. Account Creation & User Onboarding

The onboarding flow must be frictionless yet compliant. Users should be able to sign up using mobile/email authentication, followed by identity verification. Integrating eKYC solutions enables quick document verification (PAN, Aadhaar in India) along with selfie-based facial matching. The goal is to reduce onboarding time to under 5 minutes while maintaining regulatory compliance. A smoother onboarding experience directly impacts conversion rates and user acquisition costs.

2. Fund Transfers & Payments Infrastructure

At this stage, your neobank should support basic money movement capabilities, such as peer-to-peer transfers and bank transfers. In the Indian context, integrating UPI can significantly enhance usability by enabling real-time payments. The backend must ensure transaction reliability, idempotency (no duplicate transactions), and proper error handling. Even in an MVP, payment flows must be robust because any failure here immediately erodes user trust.

3. KYC/AML Compliance Layer

Compliance is not optional even for an MVP. You need built-in KYC (Know Your Customer) and AML (Anti-Money Laundering) checks to verify user identity and monitor suspicious activity. This often involves third-party integrations for document verification, sanction list screening, and risk profiling. Automating these checks reduces manual overhead while ensuring regulatory readiness from day one.

Beyond these core features, a well-designed MVP also includes a basic dashboard where users can view their balance, transaction history, and account details in real time. While the UI can remain simple, it must be intuitive and trustworthy, as early users are highly sensitive to usability and security signals.

From a business perspective, this $40k–$70k investment helps you test critical assumptions such as user acquisition cost, onboarding drop-offs, transaction frequency, and early monetization signals before committing to a full-scale build. Many successful neobanks started with a tightly scoped MVP, gathered user feedback, and iteratively expanded into lending, cards, and investment products.

In short, the MVP is your proof of concept in the real world it should be minimal in features but maximum in reliability, compliance, and user experience.

Full-Featured Launch ($150k–$400k+): Multi-Currency, Lending, Investment

A full-scale neobank includes advanced features like:

- Multi-currency accounts

- Lending services

- Investment options

- AI-driven analytics

|

Component

|

Estimated Cost Range

|

|

UI/UX Design

|

$10k–$30k

|

|

Backend Development

|

$40k–$120k

|

|

Compliance & Security

|

$20k–$80k

|

|

Third-Party Integrations

|

$15k–$50k

|

|

Maintenance

|

$10k–$40k annually

|

Neobank Monetization Models That Work

Neobanks generate revenue through multiple streams:

- Interchange fees from card transactions

- Subscription plans for premium features

- Lending and interest margins

- Partnerships and marketplace integrations

A practical example is offering premium accounts with benefits like higher transaction limits and cashback rewards.

Conclusion

Building a neobank app from scratch is a complex yet highly rewarding endeavor. It requires a strategic blend of technology, compliance, and user-centric design. From choosing the right development model to implementing robust architecture and ensuring regulatory compliance, every decision plays a critical role in the success of your neobank.

We specialize in delivering end-to-end fintech solutions, helping businesses transform their ideas into scalable and compliant digital banking platforms. Whether you are building an MVP or launching a full-scale neobank, our expertise ensures faster time-to-market and long-term success.

Recognized by DesignRush as one of the Top Fintech App Development Companies, this recognition highlights our dedication to delivering innovative, secure, and future-ready fintech solutions for modern businesses.

As a trusted Banking App Development Company, businesses can rely on TechQware Technologies to build secure, scalable, and compliance-ready neobank solutions with modern fintech architecture, seamless KYC/AML integration, cloud infrastructure, and user-focused experiences that support faster launches and long-term growth. Partner with us to turn your fintech idea into a future-ready digital banking platform.

FAQs

Do neobanks need a banking license to operate?

Neobanks typically do not require their own banking license as they operate in partnership with licensed banks. However, regulatory requirements vary by country, and some neobanks may choose to obtain licenses for greater control.

What is Banking-as-a-Service (BaaS) and how does it work?

BaaS allows fintech companies to offer banking services through APIs provided by licensed banks or platforms. This eliminates the need to build infrastructure or obtain licenses.

How much does it cost to build a neobank from scratch?

The cost ranges from $40,000 for an MVP to over $400,000 for a full-featured platform, depending on complexity and compliance requirements.

What is the difference between a neobank and a digital bank?

Neobanks are fully digital and operate without branches, while digital banks are traditional banks offering online services.

How does a neobank make money?

Revenue streams include interchange fees, subscriptions, lending, and partnerships.

What tech stack does Revolut use?

Revolut uses a microservices-based architecture with modern programming languages, cloud infrastructure, and scalable databases.

TechQware

TechQware